How a Fed Rate Cut Can Lead to Higher Mortgage Rates

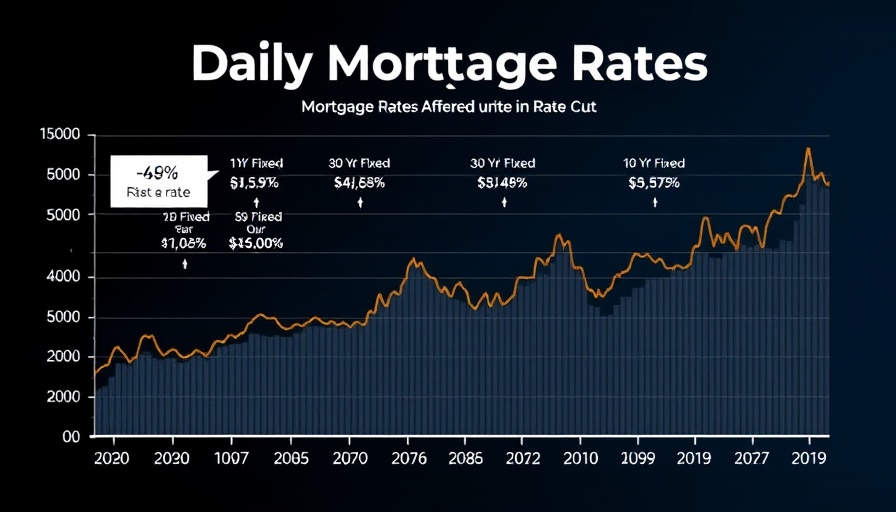

On September 17, 2025, the market experienced an unexpected turn when mortgage rates surged following a Federal Reserve rate cut. This reaction raises pivotal questions about the dynamics of interest rates and financial markets. Typically, a rate cut is intended to stimulate economic activity, yet the reality is that mortgage rates can react contrary to expectations. Understanding this phenomenon requires a closer look at the Fed's mechanisms and the roles of market expectations, economic data, and investor sentiment.

The Role of the Fed's Dot Plot in Market Reactions

The Fed's 'dot plot'—a chart illustrating the individual interest rate forecasts of Federal Reserve officials—plays a crucial role in shaping market expectations. Released alongside every rate cut announcement, this plot indicates how the Fed members foresee future rate changes. In this instance, the dot plot was interpreted as conveying the likelihood of additional cuts, which injected optimism into the bond market initially. However, subsequent comments from Fed Chair Jerome Powell signaled a more cautious approach, emphasizing that the dot plot does not guarantee future cuts and does not represent a concrete plan.

Market Volatility: Understanding Investor Behavior

The volatility seen in the mortgage rate market isn’t just about the Fed's actions but also about how investors react to anticipated economic signals. Following the press conference, bonds saw a reversal of the initial downward trend, resulting in mortgage lenders having to adjust rates upward. This underscores a significant point: investors often react not just to concrete actions but to the interpretation of future economic indicators. If those indicators suggest a volatile economic landscape, like rising inflation or changing employment rates, mortgage rates can climb, reflecting investor caution.

The Ripple Effect: High Rates Amid Lower Borrowing Costs

For homeowners and potential buyers, the implications of rising mortgage rates can be staggering. Although the Fed's actions aim to lower borrowing costs to stimulate growth, the intricate nature of the mortgage market can lead to scenarios where rates rise instead. As a result, those considering purchasing a home or refinancing could face higher costs, potentially straining budgets and leading to a slowdown in the housing market. This irony highlights the financial complexities that consumers must navigate amid policy changes.

What This Means for Consumers and Future Housing Markets

The implications of rising mortgage rates after a Fed rate cut extend beyond just individual borrowers; they can shift the dynamics of the housing market as a whole. With many buyers potentially retreating due to higher costs, housing demand may decrease, impacting home prices. Furthermore, those looking to enter the market could decide against buying, creating a ripple effect that could slow economic recovery in the real estate sector. An understanding of these market forces is essential for those contemplating a move in this intricate landscape.

Conclusion: Staying Informed as Rates Shift

As the Federal Reserve navigates through uncertain economic waters, it is essential for consumers, investors, and industry professionals alike to stay informed. The relationship between Fed decisions and mortgage rates is nuanced; what seems like a straightforward rate cut can lead to unexpected results in the housing market. Understanding these dynamics not only aids in making informed financial decisions but prepares individuals to better anticipate market movements in turbulent times.

To stay updated on mortgage rate changes and gain insights into market trends, consider subscribing to our mortgage rate alerts, ensuring that you receive timely information that can inform your financial decisions.

Write A Comment