Add Row

Add Row  Add

Add

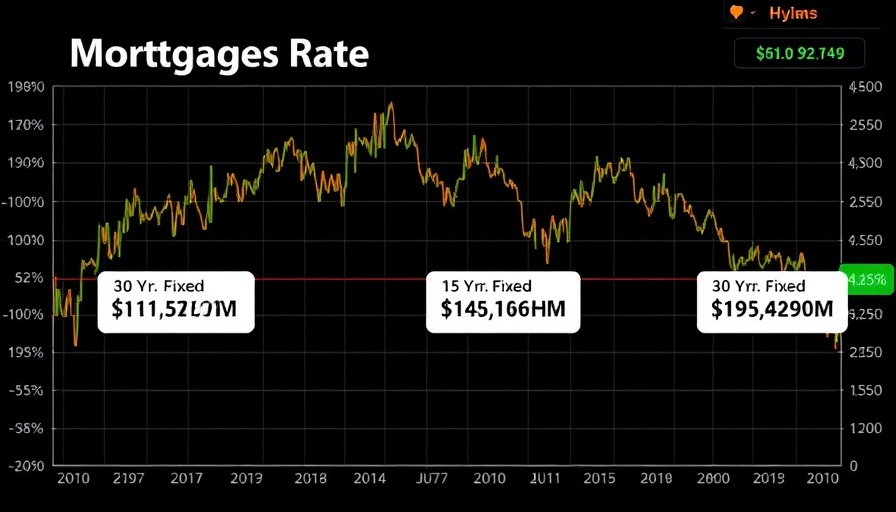

Mortgage Rates Find Stability Amid Economic Fluctuations

The recent mortgage rates trend indicates a friendly and stable environment as they have maintained a positive trajectory for more than a week. Daily breaks upward have not been noted, suggesting a temperate recovery in the bond market, particularly following the turbulence caused by the recent tariff announcements on April 2nd. For homeowners and prospective buyers alike, the re-establishment of mortgage rates into a manageable range is a positive indication, particularly when considering the broader implications of economic policies on home financing.

The Ripple Effects of Tariff Announcements

The initial wave of tariff announcements contributed to a significant spike in mortgage rates, as traders reacted to their potential economic repercussions. Financial markets often experience a degree of panic during such announcements, which can lead to short-term volatility, especially within the bond market. However, the response from the trading community has evolved as confidence in a balanced trade approach grows, allowing rates to stabilize. Understanding this cyclical behavior equips buyers with the knowledge to navigate through potential market shifts effectively.

Inflation Pressures and Economic Expectations

While the immediate stabilization of mortgage rates is encouraging, inflation concerns linger. The debate adequately revolves around whether tariffs will lead to a rise in inflation and how that impacts borrowing costs. Typically, as inflation rises, so do mortgage rates, presenting a dichotomy that borrowers should consider. Today’s modest victories in mortgage rates may be fleeting unless economic fundamentals—including inflation and trade agreements—align favorably. For borrowers, remaining informed about these fluctuations provides timing leverage in their financing decisions.

Fostering Resilience in Home Buying

In light of these observations, home buyers should maintain a proactive stance. Factors such as monetary policy, consumer confidence, and inflation projections are instrumental in determining future mortgage rates. By being aware of these influences, potential buyers can better time their purchases for optimal conditions. Additionally, utilizing tools like market monitors and rate alerts, which are more accessible than ever, can help home seekers develop a strategic approach to purchasing their homes, ensuring they capitalize on favorable rates when available.

Looking Ahead: Predictions for Mortgage Rates

The journey of mortgage rates in the coming months appears complex yet promising. As markets adjust to new economic realities post-tariff adjustments, mortgage rates will continue to oscillate based on underlying economic data. Observers should watch for monthly inflation data and economic growth reports that could influence interest rates significantly. By being attuned to these key indicators, stakeholders can navigate home financing with greater clarity and confidence.

Practical Steps for Consumers

Stay Updated: Regularly monitor financial news and subscribe to rate alerts to gauge market conditions. Knowledge is power in making informed decisions, particularly in a fluid market environment.

Consider Long-Term Implications: While current rates are stable, assessing future economic indicators like inflation can help determine the longevity of favorable rates. Weighing the pros and cons of fixing rates now versus waiting can lead to more financially sound choices.

Conclusion: Seizing the Opportunity

With mortgage rates on a steady upward trajectory and economic policies evolving, now is the opportune time for consumers to stay informed and proactive in their home buying journey. As always, remaining educated and vigilant about potential fluctuations can lead to more significant financial benefits in the long run.

Write A Comment